Mission Federal Credit Union is committed to serving San Diego County. In fact, Mission Fed is the largest locally based financial institution exclusively serving San Diego County. We know many of our members have unique needs, so we wanted to hear from our community about their credit habits. To learn more, we surveyed 400 San Diegans, ranging in age from 25 to 54, to find out how they use their credit cards and how Mission Fed, as a financial institution prioritizing people over profit, can help.

Our key survey findings

- 65 percent of participants claim to use their credit card for necessary items or emergencies only

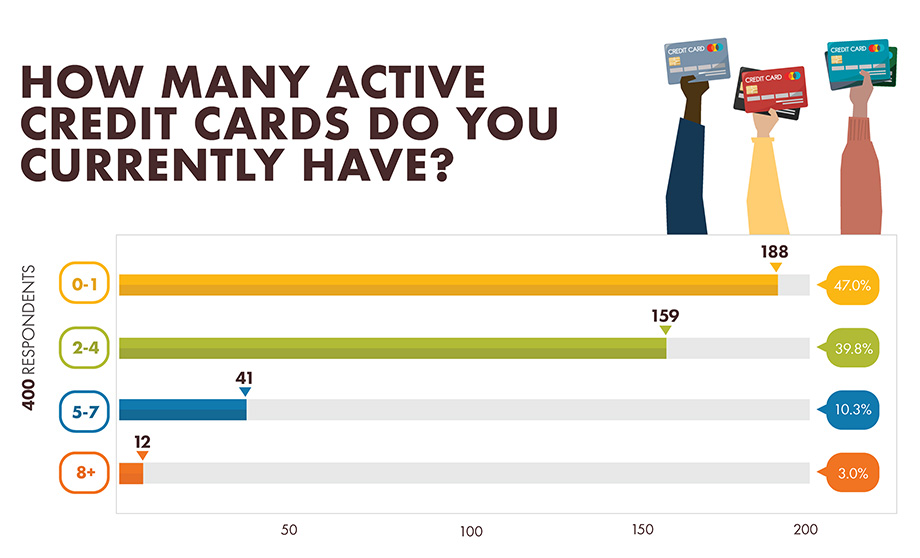

- 47 percent of participants prefer to keep a small number of credit cards, and only maintain 0-1 credit cards

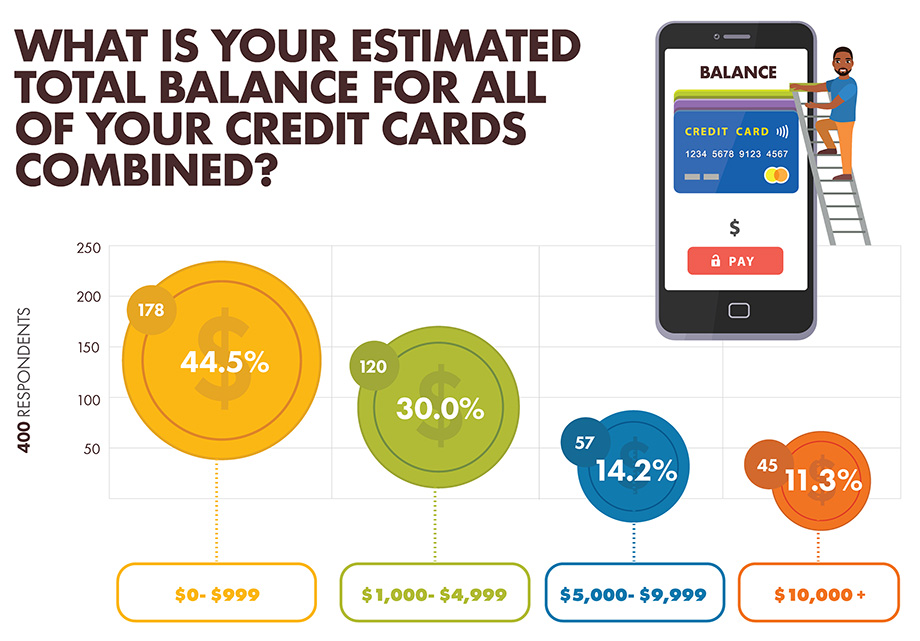

- While over 44 percent of participants had less than $999 in credit card debt, 11 percent had over $10,000 in credit card debt

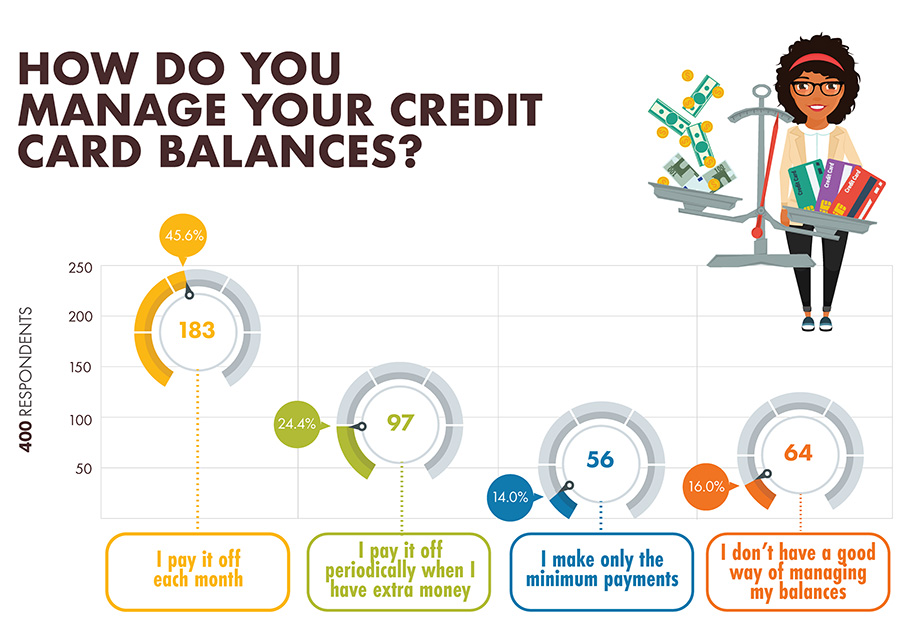

- 45 percent of participants pay off their credit card balances in full each month

- Almost 24 percent of participants are anxious about their credit card debt causing them to worry and lose sleep

How San Diegans use credit cards

Credit cards are helpful and can come with great perks like rewards and cash back, but it’s important to know how to use your credit cards wisely—otherwise, credit card debt could affect your credit score and credit history if not paid in a timely manner.

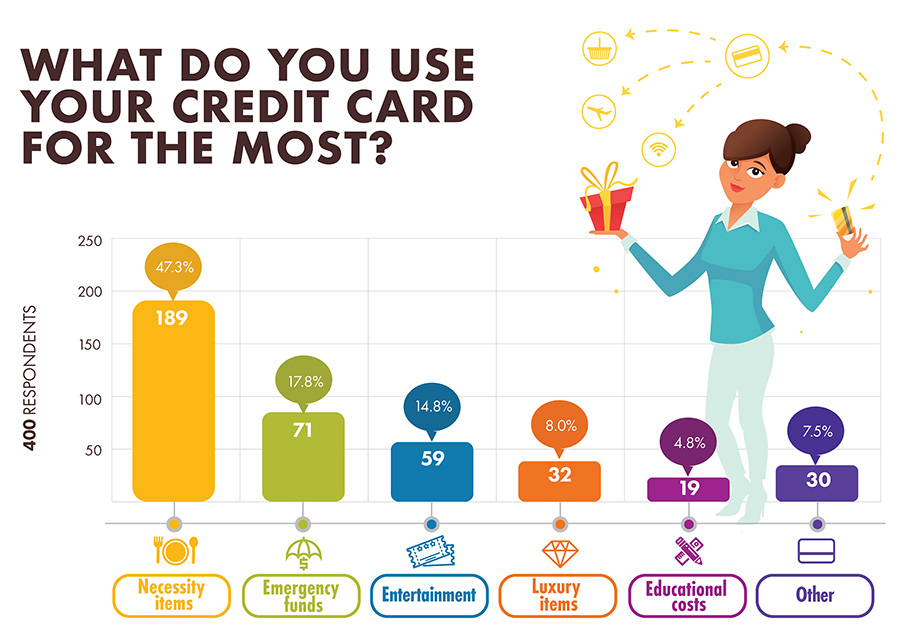

We wanted to know how our community uses credit, so we asked our survey participants what they use their credit cards for.

The majority of San Diegans surveyed—65.1 percent—said they use their credit cards for necessary items or for emergency funds. We asked Millie Garland-D’Aprile, Vice President, Operations, why people would choose to use credit for everyday necessities. “Many people like to use one payment method for all their bills and necessities. It streamlines their purchase history and makes it easier to review. Plus, they’re able to earn rewards quickly if their credit card carrier offers a reward program,” she answers.

At Mission Fed, we offer the Mission Rewards Credit Card reward program, available with eligible credit union Credit Cards. This reward program offers:

- A variety of rewards to choose from like cash back, gift cards and more

- Bonus points for shopping with select merchants

- No booking fees to redeem travel rewards

- Easy access to check and redeem points within Online Banking

- Points that won’t expire if you use your eligible Mission Fed Credit Card at least once every two years

Members with Credit Card enrolled in Mission Rewards can quickly build points and redeem them for cash back, gift cards, travel deals, airline tickets, green products and more. Even better, members who pay their balance each month can enjoy the rewards without building excess interest—that’s smart spending.

San Diegans may want different cards, depending on their benefits, for any number of uses and purposes. Make sure you have the right card for your needs. With our Preferred Platinum Credit Card, you can earn even more benefits at a low interest rate.

When is it beneficial to have more than one credit card?

It’s common to think it’s best to avoid getting a credit card or to maintain just one credit card, but is that what’s best for your credit history? As it turns out, your credit history can actually benefit from having multiple credit cards if you use them properly. Let’s explore why.

When we surveyed San Diegans, 47 percent of participants had 0-1 active credit cards. That may seem responsible because it makes it harder to overspend, but it’s not necessarily the amount you spend that matters. When it comes to your credit score, 30 percent of your score is decided based on your debt utilization ratio, or the amount of your available credit that you use. To maintain a positive credit score, you should use no more than 30 percent of your available credit. If you only have one credit card, that can be harder to maintain, resulting in a higher debt utilization ratio.

Is it better to avoid credit cards all together? While it might seem that way, it’s difficult to build an adequate credit history without a credit card. Mission Fed’s Vice President, Card Services, Lori Koscki reminds us, “Responsible credit card use is good for your credit score, and when you choose the right card for your needs, it can even help you build up rewards for things you need.”

How to choose the right card for you

Ideally, each credit card you have is helpful for different things. Your first step is to consider how you’ll be using your credit card, as well as whether you’ll be able to pay it off completely each month. Here are some options to consider:

- If you’re just getting started or trying to revive your credit:

Find out what your credit score is currently. If you don’t have an established credit history or discover your credit score is lower than you’d like, the right card and responsible use can help you improve your credit score. Another option is to try a secured credit card, which is often tied to a savings account and allows a spending limit the size of that account or smaller, generally $300 to $500. You’ll use the card normally like a regular credit card, and lenders will feel secure because of the money in the connected savings account. While Mission Fed offers low interest rates, be sure to read the fine print about any rate increases, and be conscientious about paying your balance off on time each month. - If you’re using a credit card to purchase most of your necessities:

Look for a card that offers rewards with frequent use. A Credit Card like Mission Fed’s Preferred Platinum Mastercard® can offer a low APR plus rewards, and is perfect to use as your primary credit card. Look for introductory offers, too, to get bonus points and a low or 0% introductory APR for a fixed period. This is a great Credit Card for balance transfers. However, it’s still important to continue to pay off your card on time as your payment history accounts for 35 percent of your credit score. - If you travel frequently:

Consider a travel-specific card to make it easier to keep track of expenditures. Credit cards are more secure, too, because they’re not attached to your checking or savings accounts and you’re less likely to be held responsible for fraudulent charges. Consider reloadable travel cards for backup. Mission Fed offers Visa TravelMoney® Reloadable Cards for your convenience and security, offering Zero Liability Protection, 90-day purchase protection, travel and emergency assistance and lost luggage reimbursement. Since the card isn’t tied to any of your accounts, you won’t have to worry about credit card fraud. Just load the card with your desired amount, up to $5,000, as needed.

What to do if you have significant credit card debt

While most of us try to avoid carrying a lot of credit card debt, it’s not always possible. We asked our survey participants to estimate their total credit card balance, and 11 percent of those surveyed are living with more than $10,000 of credit card debt.

If you end up in this situation, what should you do?

- Make a plan for repayment

If you have a lot of credit card debt, figure out how much you can afford to consistently pay each month, without ever missing a minimum payment. Late or missed payments negatively impact your credit score, costing you more in higher interest rates and potentially causing you to be denied for future credit. - Figure out how long it will take you to pay off the balance

It’s important to try to pay more than the minimum payment to bring your balance down. The minimum payment only pays interest, so your balance continues to grow with added interest if you can’t pay more than that. Take a look at the bottom of your credit card statement and pay close attention to the amount of time you’ll need to pay when making the minimum payments versus a larger payment. Mission Fed’s Vice President, Controller, Steve Hasbrooke says, “If you can pay more than the minimum, you’ll cut the time you’re paying significantly and save yourself a lot of money.” Look at the examples below, or use this Mission Fed Credit Card Pay-Off Calculator to figure out how long it’ll take you to pay off your debt. - Online calculator tools can help you

Use this Mission Fed Credit Card Pay-Off Calculator to figure out how long it’ll take you to pay off your debt. Below are some examples of how you could pay off your debt. Note these are examples only and do not reflect your actual payment amounts or payment timelines. - Paying only the minimum monthly payment:

Credit card balance = $10,000

Annual percentage rate = 10 percent

Minimum monthly payment = $200

Years to payoff credit card debt = 5.42 - Paying more than the minimum monthly payment:

Credit card balance = $10,000

Annual percentage rate = 10 percent

Monthly payment = $400

Years to payoff credit card debt = 2.33

If you don’t pay your balance in full each month, you will accrue interest. Paying more than the minimum balance each month can save you money and help you pay off your debt sooner. Of course, in order to pay off your debt, you have to commit to no longer using your credit card until you can pay off the balance in full each month.

If you can’t pay more than the minimum, look into debt consolidation

Debt consolidation allows you to roll high-interest debt, like credit card bills, into one lower-interest payment, making your monthly bills more manageable and reducing your total debt. There are several ways to do this:

- Open a new credit card with 0% introductory interest on balance transfers

Transfer all your balances onto this card and commit to paying it off before the 0% introductory interest period ends. - Get a fixed-rate debt consolidation loan

Use the money from the loan to pay off your debt, then pay down the loan as quickly as possible over the set term. - Take out a home equity loan or 401(k) loan

Use the loan to pay off your debt, then repay the loan as quickly as possible to renew your equity or 401(k).

Each of these methods carries some risk if you’re not responsible and reliable with your payments. However, if you commit to timely payments, debt consolidation could allow you to accrue less interest and pay off your debt faster.

Mission Fed offers 0% Introductory APR for 12 months on purchases and balance transfers posted within the first 90 days of opening a new Mission Fed Platinum or Preferred Platinum Mastercard Credit Card. After that, the standard APR for Preferred Platinum Credit Cards will be 9.90% for purchases and 11.90% for balance transfers; and for Platinum Credit Cards, 11.90% for purchases and 13.90% for balance transfers. The balance transfer fee is either $2 or 2% of the amount of each transaction, whichever is greater. If you have credit card debt you’d like to pay down quickly, take advantage of this offer and pay down—or pay off—your credit card debt without paying additional interest. Once you’ve paid down your debt, get in the habit of carrying a low balance, like the 44 percent of our survey participants who carried a balance of less than $1,000.

Good credit card habits benefit you

If you’re responsible about keeping low credit card balances and paying them off each month, you’ll save yourself a lot of money and stress, but that’s not all. You’ll also find that you reap the benefits of those good habits for years to come. We asked our survey participants about how they manage their credit card balances, and 45.3 percent of those surveyed said they pay off their card each month. Well done, San Diegans!

When your credit history reflects timely payments and fully paid balances each month, lenders can see that you’re responsible with your credit. As a result of your carefully cultivated credit score, you’ll see any number of perks, including, but not limited to:

- The ability to be approved for loans when you need them

- Approval for larger loans that others might not qualify for

- Lower interest rates

- Higher limits on credit cards

- The ability to negotiate lower interest or better terms

- Better car insurance rates

It feels good to be responsible, but it feels even better to be rewarded for being responsible. Great credit habits mean you’ll have access to larger lines of credit and lower interest rates when you need them, but won’t be haunted by large balances.

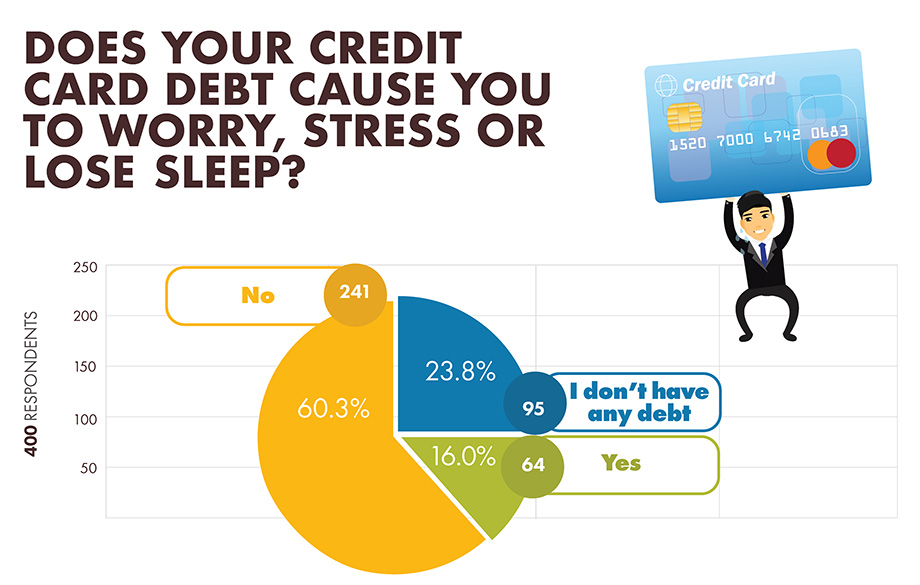

Don’t let your credit card debt keep you up at night

Carrying debt is stressful, and when you know your credit card balance is accruing interest and growing daily, you could even lose sleep over it. We wondered if credit card debt causes San Diegan consumers to worry, stress or lose sleep, and we discovered that, while 60.3 percent of our survey participants said they didn’t worry about their credit card debt, 23.8 percent did.

Of the 95 people who said they lose sleep, worry or stress about their credit card debt, only 26 paid it off each month. That means 69 of those participants continued to carry a balance month to month, which only adds to the stress and worry.

Mission Fed can help you reduce stress associated with credit card debt

Mission Fed works hard to make sure we meet customers’ needs and we do everything we can to make holding a Credit Card with us as stress-free as possible. Our excellent customer service and convenient, competitive products offer advantages like:

- No or low annual fees

- Low interest rates

- Promotions with special offers, like this Credit Card Promo offering:

- 0% Introductory APR for 12 months on purchases and balance transfers made in the first 90 days of opening a new Mission Fed Platinum or Preferred Platinum Mastercard Credit Card

- After that, the standard APR for Preferred Platinum Credit Cards will be 9.90% for purchases and 11.90% for balance transfers; and for Platinum Credit Cards, 11.90% for purchases and 13.90% for balance transfers

- The balance transfer fee is either $2 or 2% of the amount of each transaction, whichever is greater

- Mastercard benefits, including:

- Zero Liablity

- ID Theft Alerts™

- Travel Accident Insurance

- Price Protection

- Identity Theft Resolution Services

- Extended Warranty

- Mastercard® Global Service™

- Priceless Cities

- Year-end Summary Statements, including fraud detection alerts

- MasterRentalTM Insurance

- Mastercard® SecureCode™

- Daily Credit Card Purchase Money Match drawings up to $250—learn more about our $1 Million Mission Fed Money Match

- Mobile Wallet payments, allowing you to securely store and use your credit card information

If you’re still worried about your credit card debt, Mission Fed is here to help. Hasbrooke comments, “Our knowledgeable employees can point you toward tools, services and resources to help you get on top of your debt. We’re here to help you get organized every step of the way.”

Start by using our Calculators to help you take charge of your debt. You can calculate:

- Your loan payment

- How extra payments will affect your loan

- How long it will take to pay off your credit card(s)

- How long it will take to pay off your loan

- Whether or not you should consolidate your debt

Next, make an action plan to pay off your credit cards:

- Organize your expenses and make a budget

- Get creative with your payment schedule

- Pay as much as you can as often as you can

- Simplify your debt by consolidating

After that, expand your understanding of credit by reviewing our comprehensive Credit Guide. You’ll learn more about how credit works and how to establish good credit, maintain a positive credit history and repair your credit when necessary, along with what to do about credit fraud.

Mission Fed surveyed San Diegans about their credit habits to better understand how they’re using credit cards, and how we can help. We put people over profit because at Mission Fed, your success is our bottom line. Stop by any of our branches today to discuss your credit habits, and find out how we can help you.

The content provided in this blog consists of the opinions and ideas of the author alone and should be used for informational purposes only. Mission Federal Credit Union disclaims any liability for decisions you make based on the information provided. References to any specific commercial products, processes, or services, or the use of any trade, firm, or corporation name in this article by Mission Federal Credit Union is for the information and convenience of its readers and does not constitute endorsement, control or warranty by Mission Federal Credit Union.